FADA President, Mr. C S Vigneshwar, shared his perspective on the auto retail performance for September 2024, stating, “The 2024 southwest monsoon recorded 8% above-normal rainfall—the highest in four years—which has boosted Kharif sowing by 1.5% YoY. This increase in agricultural productivity has positively impacted rural demand and economic sentiment.

Despite the onset of festivals such as Ganesh Chaturthi and Onam, Dealers have reported that the performance has been largely stagnant. This suggests that overall market sentiment during these festive periods has been underwhelming, with a trend leaning towards flat or negative growth.

The Shraddh period further impacted sales negatively, leading to a YoY decline in retail sales across various categories. Discounts and offers have been introduced across segments to stimulate demand, but these have yet to translate into a significant improvement in sales.

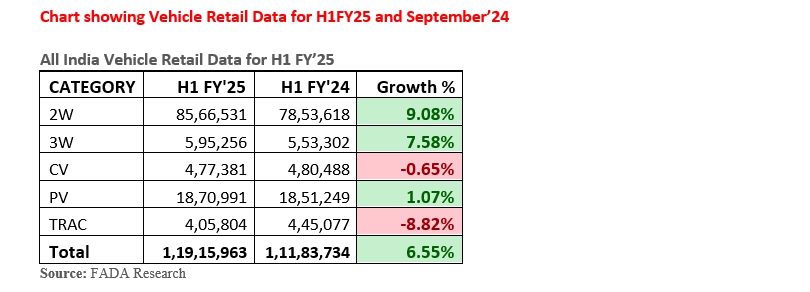

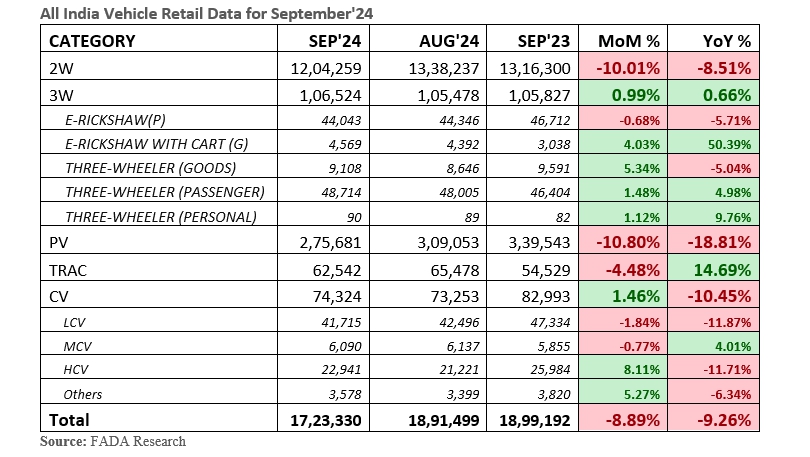

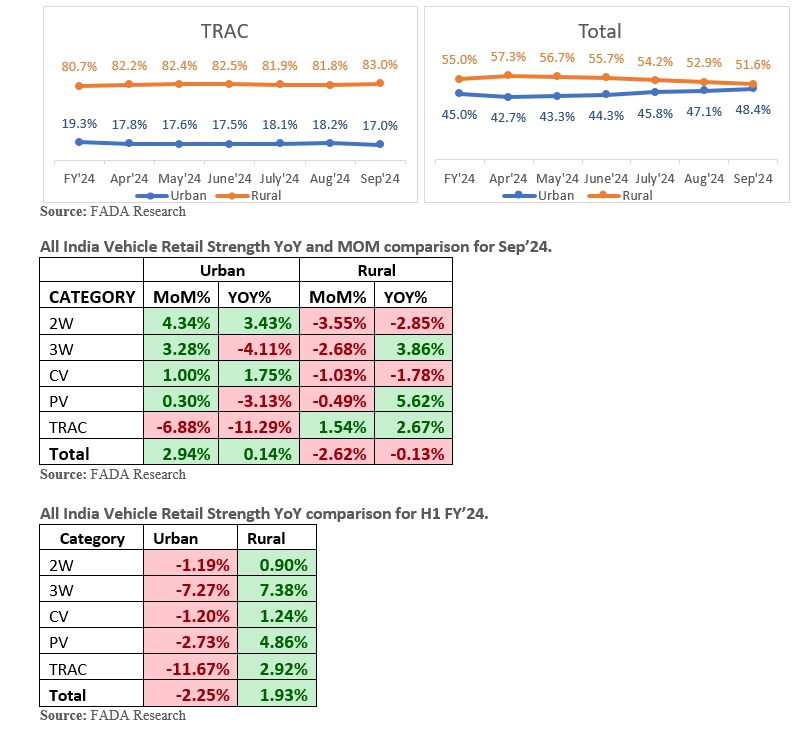

September saw a decline in overall retail sales, dropping by 9.26% YoY. Except for 3W and Trac, which grew by 0.66% and 14.69% YoY respectively, other categories such as 2W, PV and CV fell by 8.51%, 18.81%, and 10.45% YoY, respectively.

The 2-wheeler sales declined by 10% MoM and 8.5% YoY due to low consumer sentiment, poor inquiries, and reduced walk-ins. Seasonal factors like the Shraddh period, Pitrapaksha, and heavy rains further impacted demand, resulting in delayed purchases and a subdued market environment.

The 3W sales showed marginal growth of 0.99% MoM and 0.66% YoY, driven by positive customer engagement and increasing demand for e-rickshaw options. However, overall demand remained subdued as many customers deferred purchases in anticipation of the upcoming festive season and heavy rains impacted walk-ins and sales activity.

CV sales increased by 1.46% MoM but declined by 10.45% YoY, reflecting mixed performance. While there was positive sentiment and marginal growth in regions supported by infrastructure projects, overall demand remained weak due to low government spending, extended monsoon delays and seasonal challenges. Despite some improvement in fleet purchases, the market conditions remain subdued.

In the PV category, sales plummeted by 10.8% MoM and 18.81% YoY, signalling an alarming trend of declining consumer demand and deteriorating market sentiment. Seasonal factors such as Shraddh and Pitrapaksha, coupled with heavy rainfall and a sluggish economy, have exacerbated the situation, leaving Dealers with historically high inventory levels of 80-85 days—equivalent to 7.9 lakh vehicles worth ₹79,000 crore.

Given the critical festive season around the corner, FADA urges OEMs to take immediate corrective measures to avoid a financial setback. FADA also calls on the Reserve Bank of India to issue an advisory to banks, mandating stricter channel funding policies based only on Dealer consent and on actual collateral, to prevent Dealers from facing additional financial pressure due to unsold stock. This is the final opportunity for PV OEMs to recalibrate and support market recovery before it’s too late!”

Near-Term Outlook

The near-term outlook for Automobile Retail is cautiously optimistic as both Navratri and Diwali fall in the same month, creating strong expectations for a surge in vehicle sales. With healthy water levels in reservoirs and improved crop yields supporting rural demand, the festive season is expected to drive a substantial boost in 2W, PV, and Trac sales with new launches been planned for the month. However, the PV segment faces a critical situation due to high inventory levels at dealerships. If sales do not pick up as expected in October, Dealers could face significant financial pressure from unsold stock piling up in their warehouses.

While Dealers and OEMs are betting on robust festive sales, especially in rural markets where positive cash flow and better agricultural conditions are expected to spur demand, the outcome remains uncertain. A successful October is essential to clear out excess inventory and set a positive growth trajectory for the remainder of FY25. With rising inquiries and optimistic Dealer sentiments, the outlook leans towards optimism, but high stakes and dependency on October’s performance warrant a cautious approach. If the anticipated sales do not materialize, it could shift the outlook to pessimistic, putting Dealers as well as OEMs in a difficult position heading into the new year.

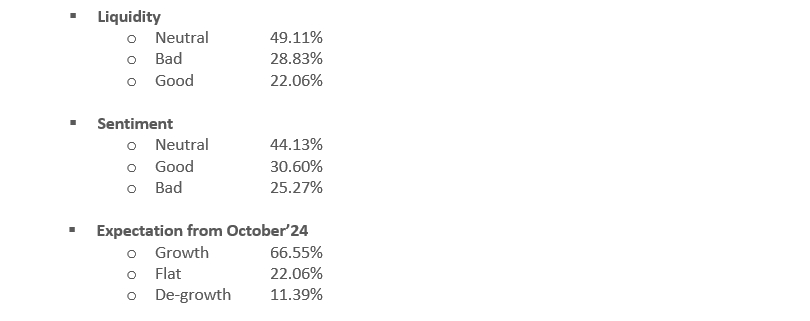

Key Findings from our Online Members Survey